The governments of the United States of America (USA) and China ultimately agreed on the first phase of their long-anticipated trade agreement around the middle of December 2019. This was a significant step for the two nations that have, for some time, been locked in a trade war of actions, if not words. Because China and the USA are the two largest economies on the globe, any trade skirmishes between them would have significant implications for the rest of the world. The new limited deal included a commitment by the U.S. government to cancel all the import tariffs that were anticipated at the end of the month. Additionally, the USA reduced some of the tariffs that it had already put in place. For its part, the Chinese government agreed to purchase $50 billion worth of farm imports from the USA as well as tightening intellectual property systems.

Cancellation of Import Tariffs

Many businesses that are currently involved in shipping and transportation were relieved by the news that import tariffs were being moderated. This was welcome news after the trade war has significantly affected the volumes and viability of the two industries. At the same time, some were sounding a tone of caution, given the fact that many of the outstanding issues in the trade dispute were yet to be fully negotiated. That is why it is not entirely clear that after this agreement, things will go back to normal. Indeed, some are suggesting that the new normal will comprise trade skirmishes and fluctuating fortunes for those that are involved in shipping or international transportation in general.

History of Changes

These changes mark a turning point in a trade dispute that has preoccupied geopolitical analysts and nations for the best part of the last two years. On the 8th of March 2018, US President Donald Trump announced import tariffs of 25% on steel and 10% on aluminum, except imports from Mexico and Canada. Ten days later, 45 U.S. trade associations urged restraint on the basis that a trade war could harm the U.S. economy. On the 1st of April, China increased tariffs to 25% on 128 USA products. Three days later, Trump proposed 25% tariffs on 1300 products representing $50 billion worth of imports. One day later, China announced an additional 25% tariffs on 106 US products worth $50 billion. Notification of a dispute was sent to the World Trade Organization on the 5th of April, triggering a 60-day resolution requirement. During that phase, Trump considered additional tariffs worth $100 billion unless China improved its intellectual property protections.

All these changes put in motion forces that are not likely to be defeated that easily in the short run, even if there is a partial trade agreement and signs of better negotiations in the future. Certainly, the players within the industry will continue to deal with the fallout of this trade dispute for years to come. A case in point is how Beneficial Cargo Owners (BCOs) have received yet another lesson in the dangers of excessive specialization and a lack of diversification in their supply chain. The China-US dispute is a sign of the times and will lead to incremental changes that will alter the character of the international shipping and transportation industries. The history of this industry has already given us insights into what might happen if the trajectories continue as they are at the moment.

2002 U.S. West Coast Ports

One of the early examples of upheavals in the industry started in 2002 when U.S. West Coast ports suffered an extended lockout and lockdown. The dispute this time emanated from discussions about a new contract that was due to come into play concerning the International Longshore and Warehouse Union or ILWU. Within weeks, operations had slowed down, and customers were complaining of unbearable delays. An agreement was reached towards the close of July 2002 and ratification took place the next month. Six years of relative peace followed the resolution of that conflict.

Meanwhile, the docks were changing, and the business was changing with new and complex imports taxing existing infrastructure and systems. The “normal” had shifted, and that would change how the industry operated.

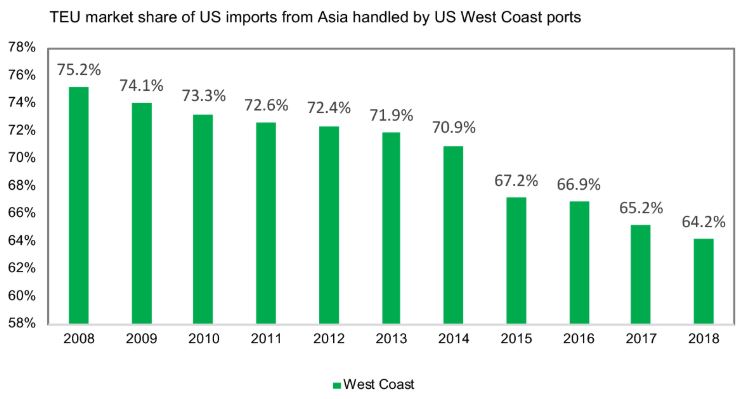

2008 Market Share Drops

When the contract was due to be renewed in 2008, there was concern that the issues experienced in 2002 would be repeated. It seemed that that would be the case when there was a one-day walkout for ports on the West Coast on May Day 2008 apparently in protest against the USA war in Iraq. Even though the old contract had formally expired on the 1st of July 2008, the union continued with its negotiations, and the cargo flows were not severely disrupted.

Perhaps this ability to handle a potentially tricky situation was a consequence of the BCOs indicating that they were ready to move on and would not tolerate being held to ransom by labor unions. Others felt that the industry had to have alternatives to the existing arrangements, and those ended up voting with their feet. Any prudent importers would try to diversity their port routing strategies so that they were not caught off guard again.

During those delicate times, the TEU market share dropped for Long Beach and Los Angeles as well as the entire U.S. West Coast during the first part of 2008. Analysis has shown that the ground that was lost was never recovered and is unlikely ever to be improved. Currently, there has been a steady drop in the proportion of container imports that are handled by the U.S. West Coast. Consequently, BCOs pivoted away from dependence on the West Coast. Instead, they adopted four and five-corner import strategies. The strategies included creating inland facilities and connections, which were then fine-tuned to service the industries.

Source: IHS Markit

BCO Danger in 2020

At the start of 2020, BCOs once again have to contend with upheavals in their industry and a harsh reminder about the dangers of poor diversification policies. This time, it is a case of over-depending on China for certain sourcing products. Some businesses have responded to this problem by shifting to other locations such as India, Mexico, and Southeast Asia. Nevertheless, it is essential to note that all these alternatives come at a cost. Some of the issues that might arise include political instability, poor infrastructure, low capacity, and an unskilled workforce. It is likely to take years rather than months to resolve these problems adequately.

The creation of five-corner import strategies will remain one of the most essential preventative and responsive actions that a business can take. It is now undeniable that the shipping and transportation industry has changed for good. BCOs can no longer place all their bet on a one-party state that has protectionist policies. A more sustainable long term model is required.

What Shippers Can Do

Offshoring products to China is no longer as straightforward as it once was. Instead, complicated decisions have to be made which balance out the risks that are involved. Currently, there is no expectation that import TEUs will outpace domestic GDP gains regardless of the economic sector that is being considered. That means that trade is a lot more complex and fragmented. One of the options that shippers may consider is nearshoring or even on-shoring to mitigate against the risks of offshoring.

One Comment on ““Asia-US Container Import Strategies Changing Despite Phase One Trade deal””

very good observation,informative.thanks a lot